When Prediction Markets Break

How a prediction market can keep trading, keep moving, and still become a worse information signal.

Chuan August Sun · Institute of Lucidity

A prediction market does not have to halt to fail. It can keep trading, keep printing volume, keep attracting attention, and still become a worse information signal.

That is the failure mode I care about. The visible market still looks alive, but price stops tracking latent truth and starts tracking crowd behavior.

Failure Is Not Always a Halt

When people imagine market failure, they often imagine a crash, a halt, or a broken system. But information failure can be quieter. The chart still moves. Traders still trade. The market still looks alive.

The failure is that price becomes a worse signal.

The Basic Metric

The arena uses tracking error as the simplest visible measure:

That can be aggregated into:

- mean absolute error,

- max deviation,

- high-error duration,

- recovery time,

- post-shock drift.

Three Failure Families

The first failure family is crowding. Too many agents react to recent price movement, so the price becomes a cause of the next price.

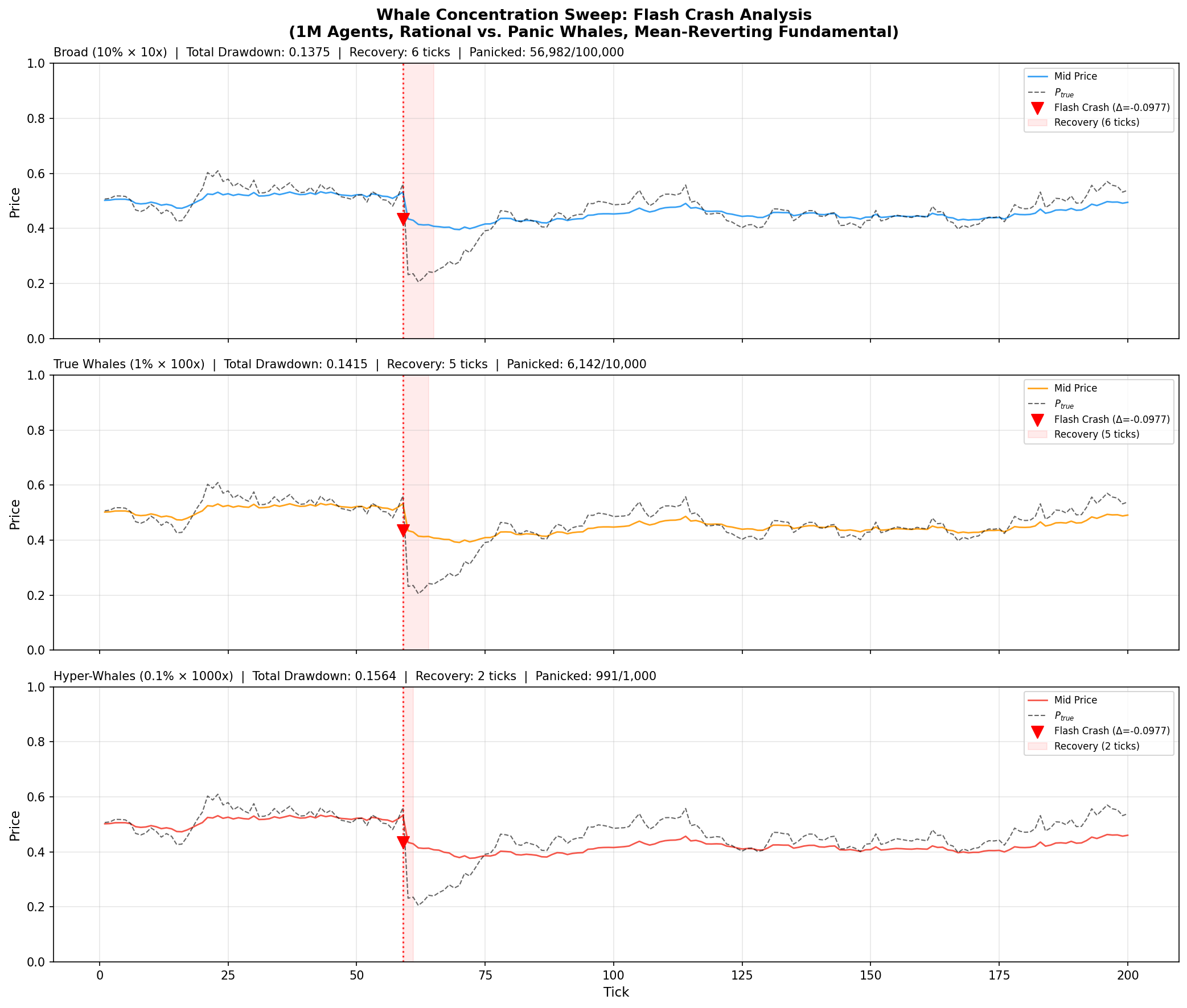

The second failure family is concentration. A small number of large positions can create asymmetric pressure and drawdown cascades.

The third failure family is synchronization. Many agents react to the same shock or signal at the same time, overwhelming ordinary liquidity.

Why the Evidence Ladder Matters

Not every result has the same status. Some results are multi-seed matched experiments. Some are single-seed stress cases. Some are browser demos.

I use an evidence ladder for this reason:

browser demo -> stress case -> matched experiment -> paper claim

The hierarchy keeps the writing vivid without becoming sloppy. A browser demo can teach the shape of a failure. A matched experiment decides whether the claim deserves to enter the paper.

What the Arena Adds

The arena lets a reader create a local failure and inspect it. Add trend followers. Add a liquidity shock. Add panic traders. Then watch price, spread, volume, stress, and commentary respond.

That experience is useful because it teaches the shape of the failure, not just the final metric.

The next question is whether arbitrage fixes the problem. The short answer is: sometimes, but only when correction has enough capacity at the moment the market needs it.